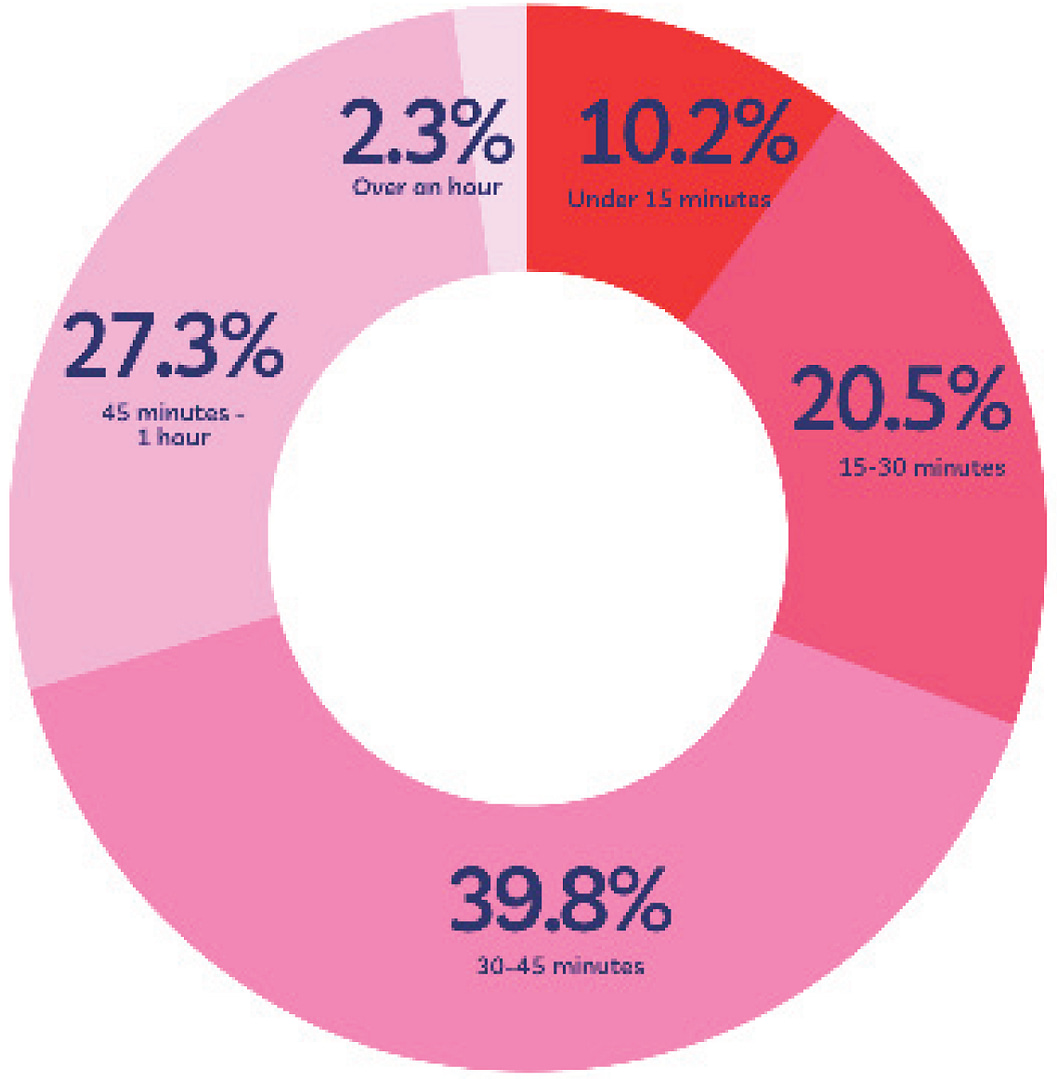

Financial literacy is a skill that in today’s ever-changing society is becoming more and more important. As high school students progress into their college years, the need to be able to cope with the financial challenges presented by independent living is paramount.

70% of college students graduate with student loan debt, with the average amount of debt arriving at $30,000, and the United States as a whole has around $1.6 trillion in student loan debt. Debt advisors like the iva-advice can help with debt problems.

Many take on debt with high interest and very little leniency and don’t realize how damaging it can be to their future lives. Furthermore, in a society where young adults are taking on credit cards without knowing the downside to such a commitment, one in four college students leave having near $5,000 in credit card debt.

Students simply don’t know basic financial necessities such as the difference between apr and interest, or what a Roth IRA is, or even why you need a good credit score, and why it is even important in the first place. Most students can’t even tell the difference between a debit or credit card.

Far too often, these students make mistakes that could simply have been avoided if they had been taught financial literacy courses. These courses teach students how to manage credit, budget, and invest money, all whilst teaching them not to make the common mistakes that their peers may otherwise have.

Students with financial literacy often appear to have a head start in life, avoiding punitive debt and getting lifelong assets much earlier than those around them.

If Loyola truly works to prepare students for college and beyond, the school needs to make financial literacy a priority for its students. The school has already created an elective, non-credit personal finance course for juniors, yet that is simply not enough.

Financial literacy affects everyone no matter the path they follow, as the need to manage one’s money is an ongoing pursuit. Therefore, as financial literacy is needed to succeed no matter what direction a student takes in life, Loyola should make every student learn at least the basics of financial literacy.

When nineteen states already require taking a course in financial literacy to graduate from high school, Loyola should be able to see the writing on the wall that what they are currently doing isn’t enough. Personal finance needs to be a mandatory course.

How can Loyola truly say it is one of the best high schools in Southern California when more than half of the graduating class doesn’t understand the fundamentals of one of the most important life skills to attain?

Comments are closed.